Introduction

In today’s volatile global economy, understanding credit ratings and credit market risks has never been more important for investors, financial institutions, and businesses. Credit ratings are more than just numbers — they reflect an entity’s ability to meet its debt obligations. In times of economic uncertainty, factors such as interest rate fluctuations, market volatility, and geopolitical tensions can directly influence credit quality and risk perception.

Primary keywords: credit ratings, credit market risks, volatile economy

What Are Credit Ratings and Why They Matter

Credit ratings are independent assessments of the creditworthiness of an entity — whether a country, corporation, or debt instrument like a bond. Rating agencies such as Moody’s, S&P, and Fitch assign scores that help investors evaluate default risk and pricing.

The key purposes of credit ratings include:

- Signaling credit risk to investors

- Determining borrowing costs in the capital markets

- Supporting proactive risk management in investment portfolios

For example, a change in the rating of a major corporation or sovereign nation can trigger significant reactions in stock markets, currency values, and bond spreads.

Key Factors Affecting Credit Ratings

1. Financial Performance and Debt Ratios

Entities with high debt ratios are more exposed if cash flow is insufficient to meet obligations. Ratings agencies evaluate profitability, liquidity, and solvency ratios to determine risk.

2. Macroeconomic Environment

Global economic conditions — such as inflation, recession risks, and central bank policies — can affect credit prospects. High inflation, for example, raises borrowing costs, increasing debt burden.

3. Political Stability and Policy Certainty

Sudden political shifts or unpredictable fiscal policies can weaken investor confidence and trigger rating adjustments.

4. Market Liquidity

A liquid market makes trading bonds or debt instruments easier, reducing liquidity risk. Conversely, in illiquid markets, selling debt securities may result in significant price discounts.

Credit Market Risks in a Volatile Economy

Credit market risks increase when economic conditions fluctuate rapidly. Key risks include:

1. Default Risk

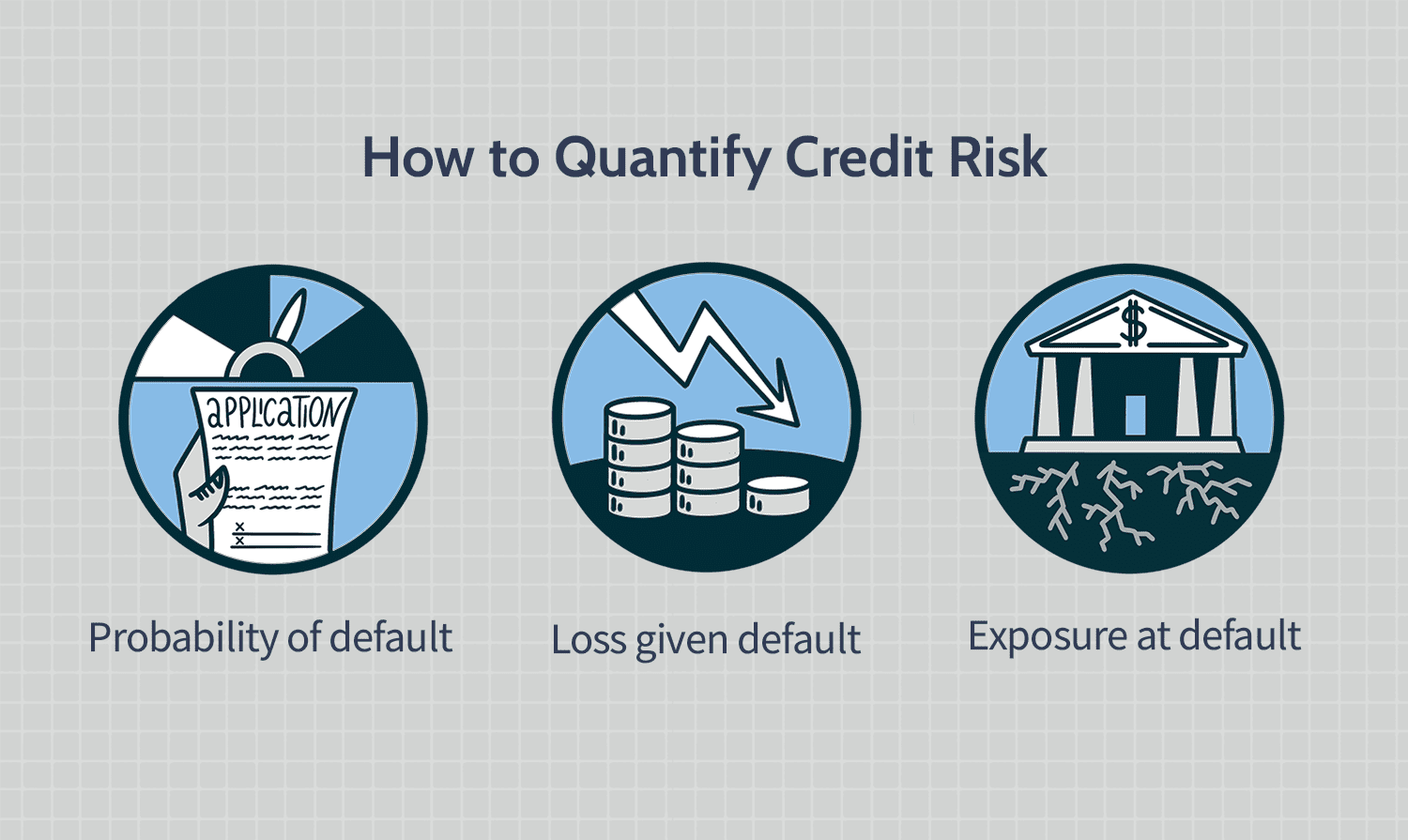

This is the likelihood that an entity will fail to meet interest or principal payments. A declining credit rating signals higher default probability.

2. Credit Spread Risk

Credit spreads — the difference between a bond’s yield and a benchmark government yield — can widen sharply during market panic, increasing the cost of capital.

3. Liquidity Risk

Investors may struggle to sell debt assets in volatile markets, potentially forcing them to accept lower prices.

4. Systemic Risk

Shock to a large company or sector can have cascading effects across the credit market, as seen during past financial crises.

How Rating Agencies Operate

Rating agencies analyze financial statements, market trends, and economic conditions to assign ratings — typically ranging from AAA (lowest risk) to D (default). While high ratings indicate safety, lower ratings signal elevated risk.

It’s important to remember that ratings are not perfect predictors. Sudden economic or political events can force agencies to revise ratings quickly.

Best Practices for Managing Credit Market Risks

Investors and financial managers can adopt the following strategies to mitigate credit risk:

1. Portfolio Diversification

Spreading investments across multiple sectors and instruments reduces exposure to a single asset’s default risk.

2. Monitor Ratings Trends

Don’t just rely on the current rating — follow trends of upgrades or downgrades over time.

3. Conduct Fundamental Analysis

Beyond external ratings, assess an entity’s cash flow, financial health, and growth potential.

4. Set Risk Limits

Use stop-loss strategies, maximum allocations per asset, and other risk management frameworks to safeguard portfolios.

Challenges During Crises and Market Volatility

Global economic uncertainties — including recessions in major economies, inflationary pressures, and geopolitical tensions — make credit predictions complex. For instance, regional policy decisions, such as the recent rejection of raw water rate reviews in Asia, can influence cross-border investment perceptions. Read also: Malaysia, Johor Reject Review of Raw Water Rates with Singapore.

Operational disruptions in major tech companies can also impact credit exposure and market confidence. Read also: Microsoft Outlook & Teams Outage Resolved After 24 Hours.

The Role of Regulators and Public Policy

Governments and financial regulators help stabilize credit markets through:

- Sound monetary policies

- Investor protection frameworks

- Oversight of rating agencies

These measures ensure transparency and reduce the likelihood of market manipulation or systemic shocks.

Conclusion

Understanding credit ratings and credit market risks is essential for navigating today’s unpredictable economy. Investors must look beyond numerical ratings and consider broader economic trends, entity fundamentals, and market conditions. Strong strategies like portfolio diversification and fundamental analysis can mitigate the impact of economic volatility and improve long-term financial outcomes.