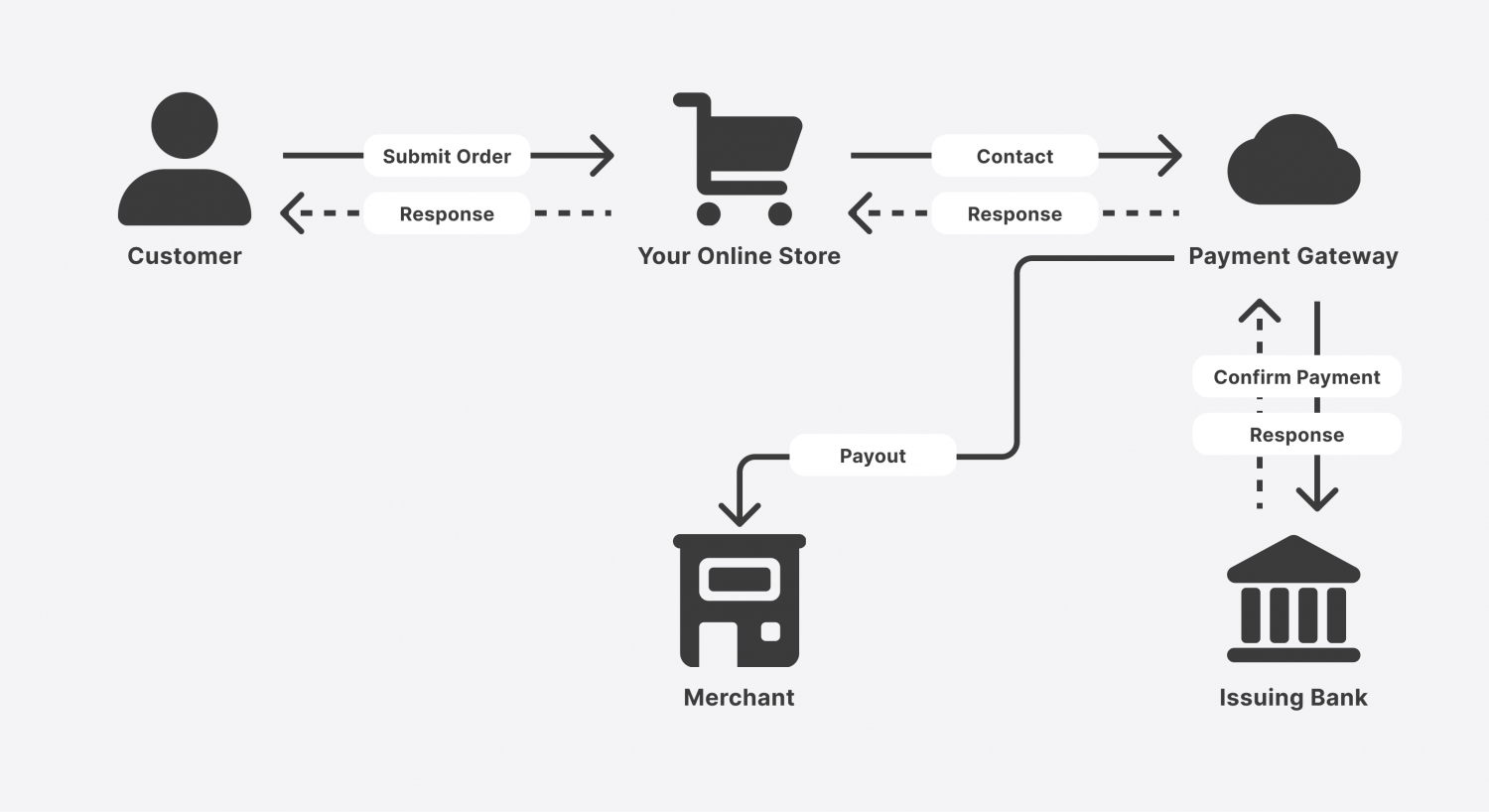

Blockchain technology, once primarily associated with cryptocurrencies like Bitcoin, has rapidly evolved to reshape modern payment systems. Its potential to provide secure, transparent, and efficient financial transactions is capturing the attention of banks, fintech companies, and even governments worldwide. As payment infrastructures become increasingly digital, blockchain offers solutions to longstanding issues, including fraud, slow processing times, and high transaction costs.

Enhanced Security and Transparency

One of the most significant innovations blockchain brings to payment systems is enhanced security. Traditional banking systems rely on centralized databases, which are vulnerable to hacking, data breaches, and human error. Blockchain, however, uses a decentralized ledger where every transaction is cryptographically secured and recorded across multiple nodes. Once a transaction is verified and added to the blockchain, it cannot be altered or deleted.

This transparency allows all participants in the network to track transactions in real time, reducing the risk of fraud. For cross-border payments, this feature is especially critical. International transactions often involve multiple intermediaries, leading to delays and opaque fee structures. By contrast, blockchain enables peer-to-peer transfers that are faster, more transparent, and cost-effective.

Lower Transaction Costs

Blockchain also significantly reduces transaction fees. Conventional payment systems impose costs at every intermediary stage—banks, payment processors, and clearinghouses each charge fees. For global remittances, these costs can be substantial, especially for small-value transactions. Blockchain eliminates most intermediaries by enabling direct peer-to-peer payments.

For instance, stablecoins—cryptocurrencies pegged to fiat currencies—allow instant transfers with minimal fees. This is transforming not only consumer payments but also business operations, especially for small and medium enterprises (SMEs) that rely on cost-efficient payment solutions to maintain cash flow and profitability.

Faster Cross-Border Transactions

Speed is another area where blockchain excels. Traditional cross-border payments can take several days due to the involvement of multiple banks and regulatory checks. Blockchain-based payment networks operate 24/7, bypassing traditional banking hours. Transactions can be completed in minutes or even seconds, regardless of the sender’s or receiver’s location.

Companies like Ripple and Stellar have been pioneers in leveraging blockchain to facilitate international payments. By reducing settlement times, businesses can improve liquidity, better manage working capital, and respond more quickly to market demands.

Smart Contracts and Automation

Blockchain’s capabilities extend beyond simple transactions. Smart contracts—self-executing contracts with the terms directly written into code—allow payments to be automated based on predefined conditions. For example, a supplier could automatically receive payment once a shipment is confirmed delivered, eliminating manual invoicing and reducing administrative overhead.

This automation reduces human error and enforces compliance, which is particularly valuable in sectors with complex contractual arrangements such as trade finance, insurance, and real estate. By embedding rules within the blockchain, smart contracts ensure that payments occur only when obligations are met.

Financial Inclusion

Blockchain also has the potential to expand financial inclusion. Millions of people worldwide remain unbanked or underbanked due to lack of access to traditional financial institutions. Mobile-based blockchain payment systems allow anyone with a smartphone to participate in the financial ecosystem.

Countries in Africa and Southeast Asia are already exploring blockchain solutions to provide affordable and secure financial services. This includes remittances for migrant workers, microloans, and even basic savings accounts. By bypassing traditional banking infrastructure, blockchain democratizes access to financial tools, promoting economic empowerment.

Regulatory Challenges and Adoption

Despite its promise, blockchain adoption in payment systems faces regulatory hurdles. Governments and financial authorities are concerned about potential misuse, such as money laundering or tax evasion. To address these concerns, many jurisdictions are developing frameworks for blockchain-based financial services that balance innovation with oversight.

Companies seeking to implement blockchain solutions must navigate varying regulations across regions, ensure compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) standards, and engage with policymakers to shape practical regulatory environments. Early adoption often requires partnerships with established financial institutions to build trust and legitimacy.

Integration with Traditional Banking

Rather than replacing traditional banks entirely, blockchain is increasingly seen as complementary technology. Banks are adopting hybrid models that integrate blockchain with existing payment infrastructures. This allows them to leverage the benefits of decentralized ledgers—speed, transparency, and security—while maintaining regulatory compliance and customer trust.

For instance, central bank digital currencies (CBDCs) are a prime example of blockchain integration in conventional financial systems. CBDCs offer the transparency and efficiency of blockchain while retaining state-backed stability, potentially reshaping monetary policy and digital payments in the coming decade.

Read Also: Seniman Muda Pelestari Budaya, Penggerak Ekonomi Kreatif

Future Outlook

The future of blockchain in payment systems is promising. As technology matures, we can expect wider adoption across sectors, increased interoperability between networks, and innovative applications beyond simple payments. Blockchain may facilitate real-time settlement of securities, streamline supply chains, and even revolutionize loyalty programs and digital identities.

Financial institutions and fintech innovators are racing to develop scalable blockchain solutions that can handle high transaction volumes without compromising speed or security. By embracing blockchain, businesses can offer faster, cheaper, and more transparent payment services, creating significant competitive advantages.

Conclusion

Blockchain is transforming payment systems by providing secure, efficient, and transparent transaction mechanisms. From lowering costs and accelerating cross-border payments to enabling smart contracts and financial inclusion, its applications are vast and impactful. While regulatory challenges remain, the integration of blockchain into traditional banking systems is paving the way for a more innovative and inclusive financial landscape. As adoption grows, blockchain could redefine how individuals and businesses interact with money, making financial transactions faster, safer, and more accessible worldwide.

Read Also: Wisata Budaya, Tradisi Lokal, dan Kearifan yang Menggugah